Housing crisis delays homeownership for young Americans

New data shows that even with solid jobs and years of savings first-buyers are still postponing home purchase.

NETHERFIELD, UNITED KINGDOM — On a spring weekend in a fast-growing American city, a young professional toured a modest three-bedroom house listed for more than $400,000. After calculating the monthly mortgage payment at today’s interest rates, the buyer realized that even years of careful saving and a stable income were not enough to make the purchase affordable.

Instead of signing a contract, the would-be homeowner left empty-handed, joining a growing number of young Americans who are postponing homeownership as soaring home prices, elevated mortgage rates, and a limited supply of affordable houses continue to reshape the path to owning a home in the United States.

Each month, Lawrence Yun reviews housing market reports that reveal how the path to homeownership has become increasingly difficult for young Americans. As Chief Economist at the National Association of Realtors, he closely monitors rising home prices, elevated mortgage rates, and a persistent shortage of affordable homes that continue to reshape the U.S. housing market.

The data show that many first-time buyers, despite having stable jobs, steady incomes, and years of savings, are delaying purchasing a home because monthly mortgage payments have climbed beyond what they can reasonably afford.

For Yun, these recurring patterns reflect more than short-term market fluctuations—they illustrate a long-term shift in which homeownership is becoming increasingly difficult for an entire generation, forcing many young adults to postpone one of life’s biggest financial milestones.

Sachi Benz in The Netherlands on June 30, 2026 at 12:41 PM. America's housing crisis affects young adults. Photo: Sachi/Latina. © Latina Studio Lens 2026

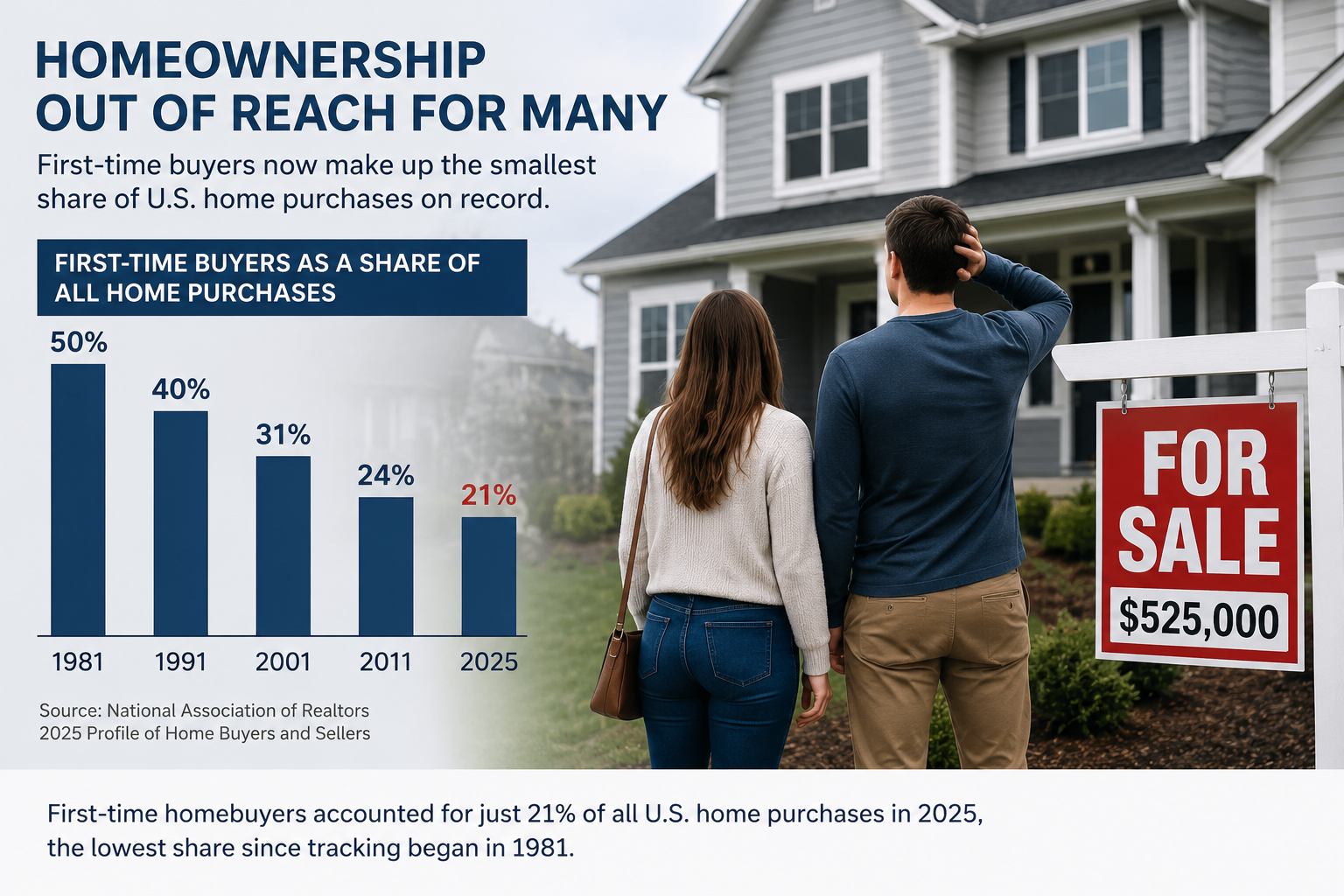

The lowest share since the National Association of Realtors began tracking the data in 1981, highlighting how affordability pressures are pushing younger Americans out of the housing market.

The same report found that the median age of first-time buyers reached a record 40 years, compared with the late 20s before the 2008 housing crisis, reflecting years of delayed homeownership. Meanwhile, the Harvard Joint Center for Housing Studies reported that existing-home sales have fallen to a 30-year low, home prices remain roughly 60% higher than in 2019, and the shortage of affordable homes continues to limit opportunities for first-time buyers.

Together, these findings show that high home prices, elevated mortgage rates, and constrained housing supply are not temporary setbacks but evidence of a sustained shift in the U.S. housing market that is delaying homeownership for an entire generation.

The housing affordability crisis has created clear winners and losers. Young Americans hoping to buy their first home are increasingly being priced out as home values and borrowing costs continue to rise, forcing many to remain renters for longer or delay major life decisions such as marriage and starting families.

At the same time, existing homeowners with low mortgage rates have benefited from rapidly appreciating property values and have little incentive to sell, further limiting the supply of homes available to first-time buyers. Real estate developers argue that restrictive zoning laws, high construction costs, and labor shortages make it difficult to build enough affordable housing, while housing advocates contend that stronger public investment, zoning reform, and expanded affordable housing programs are needed to improve access.

This growing divide between those who already own homes and those still trying to enter the market has become one of the defining tensions shaping the future of homeownership in the United States.

Housing economists expect affordability to remain a defining challenge for young Americans unless mortgage rates decline significantly and the supply of affordable homes expands. While policymakers, builders, and local governments are exploring zoning reforms and incentives to increase housing construction, progress is expected to be gradual.

In the meantime, many first-time buyers may continue postponing homeownership, reshaping when and whether they achieve one of the traditional milestones of adulthood. The question now is not only when the housing market will become more affordable, but whether the next generation will redefine the American dream if owning a home remains out of reach.